Damaging curiosity costs set world on system for most significant mass default in history

More than £2 trillion-really worth of eurozone govt bonds trade on a damaging desire charge. It truly is a bubble that is bound to end poorly &#thirteen  &#thirteen &#thirteen

&#thirteen Image: Alamy

&#thirteen

&#thirteen &#thirteen

&#thirteen Image: Alamy

&#thirteen

Here’s an astonishing statistic much more than 30pc of all authorities debt in the eurozone – around €2 trillion of securities in total – is buying and selling on a adverse curiosity price.

With the arrival of European Central Bank quantitative easing, what commenced four months in the past when 10-calendar year Swiss yields turned negative for the first time has snowballed into a veritable avalanche of damaging prices throughout European government bond markets. In the hunt for apparently “safe assets”, investors have thrown warning to the wind, and collectively identified to pay out governments for the privilege of lending to them.

On a country by nation basis, the figures are even far more startling. According to expenditure bank Jefferies, some 70pc of all German bunds now trade on a adverse yield. In France, it really is 50pc, and even in Spain, which was widely considered bancrupt only a number of many years ago, it truly is 17pc.

Not only has this never ever transpired prior to on these kinds of a scale, but it marks a scarcely believable turnaround on the situation at the height of the eurozone disaster just a small whilst back, when some European bond markets traded on yields that mirrored the quite true chance of default. However much from becoming a welcome signal of returning economic confidence, this practically surreal state of affairs truly alerts the very reverse. How did we get right here, and what does it indicate for the long term? Whichever way you come at it, the reply to this 2nd question is not very good, not excellent at all.

What can make today’s negative desire rate surroundings so stressing is this to the extent that demand is developing at all in the planet economy, it appears again to be practically fully dependent on rising stages of financial debt. The monetary disaster was intended to have exploded the credit rating bubble as soon as and for all, but there is certainly very tiny signal of it. Climbing public indebtedness has taken more than where households and firms remaining off. And in terms of wider credit growth, rising markets have merely changed Western ones. The wake-up get in touch with of the monetary disaster has long gone largely unheeded.

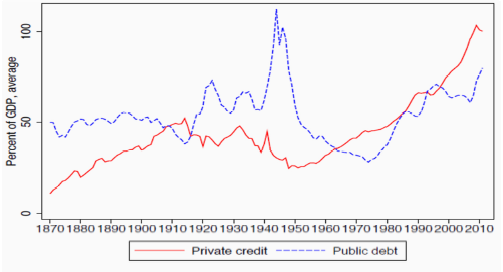

The combined community credit card debt of the G7 economies by itself has grown by shut to forty proportion factors to about 120pc of GDP given that the start off of the disaster, while globally, the total debt of non-public non-monetary sectors has risen by 30pc, considerably in progress of economic progress.

Community and non-public personal debt in sophisticated economies since 1970: Source Longview Economics

1 by one, all the key central banking institutions have joined the money printing get together. Very first it was the US Federal Reserve. Then came the Bank of England and afterwards the Lender of Japan. Just recently, it’s the European Central Bank. Now even the People’s Lender of China is contemplating the “unconventional” financial help of bond purchasing . Anything at all to keep the demonstrate on the road. It is what Chris Watling of the consultancy Longview Economics has termed the “philosophy of demand from customers at any cost”. A crisis induced by as well considerably debt has been fought with even more of the things.

Several would contend that it is central financial institution cash printing alone which is the main lead to of today’s minimal desire fee setting. Up to a point, it’s a check out that is challenging to argue with, for that is without a doubt the total function of QE – to depress the yield on federal government bonds to the position the place investors are compelled to seek out increased risk alternate options.

Other contributory factors contain “financial repression”, where ever a lot more demanding solvency regulation forces banking companies and insurers to hold more bonds, whatsoever the value. Alternatively, some element of the clarification may be down to QE having starved the repo industry of the bonds it wants as collateral, even if most central banking companies have preparations to lend the stock back again to marketplaces for these purposes.

Distortions brought on by the ECB’s €60bn-a-thirty day period of bond purchases have been notably obvious in German bunds, one of the most sought-right after types of collateral the German government’s coverage of operating a budget surplus implies that the measurement of the market is presently shrinking, with internet payback fairly than web issuance. The Bundesbank president, Jens Weidmann, has been identified privately to complain that the ECB’s bond-purchasing orders are, for Germany, a variety of Kafkaesque encounter it’s as if he’s awoken to discover he’s metamorphosed into a giant insect.

All this formal interference has no question influenced negative yields. But it also raises a further concern, which is whether or not central banking companies are the primary trigger of the collapse in curiosity rates, or no matter whether they are just accommodating broader forces in the world-wide economy that they are powerless to impact – persistent sluggishness in demand from customers and productivity expansion.

What’s result in, and what is effect? In a speech last year, Ben Broadbent, deputy governor of the Financial institution of England, argued cogently that central banking companies are simply responding to these further forces. The normal, or equilibrium, charge of interest needed to hold development and inflation at a certain level is basically a great deal reduce than it utilized to be, he insisted. To decide by the markets, it may even have turned unfavorable.

There is some assistance for this view in the way marketplaces have responded to QE. Analysis by Longview Economics discovered that bond yields actually rose throughout periods of QE by the US Federal Reserve, and fell when it stopped, the reverse of what you may anticipate if you think it is the unrestricted getting power of the central bank that is leading to the interest rate to drop.

Costs would rise during durations of QE simply because buyers envisioned it to have a constructive influence on economic development, and as a result the equilibrium price of desire, and then tumble after it stopped due to the fact the stimulus had been withdrawn. Get in touch with it “secular stagnation” – the notion popularised by previous US Treasury Secretary Larry Summers – if you like, but whatsoever it is, it really is a notably disappointed area to be. For all types of reasons, superior economies, and probably rising kinds way too, look to have run out of productivity-maximizing progress and as a result want constant infusions of economically destabilising personal debt to keep them going.

The flip aspect of the inexpensive income story is soaring asset prices. The bond industry bubble is just the 50 percent of it considering that most other property are priced relative to bonds, just about every thing else has been heading up as effectively. At some point, there will be a enormous correction, in which lenders will suffer sickening losses.

No person can notify you when that instant will arrive. We reside in an “extend and pretend” world in which economies pathetically battle among by themselves for any scraps of demand. One burst of income printing is met by one more in an in the end futile, zero-sum sport of competitive forex devaluation. As if on cue, along will come another comfortable patch in Britain’s economic recovery, with 1st-quarter growth really a bit weaker than predicted . Like a continuously receding horizon, the stage at which British isles desire rates begin to increase is pushed at any time additional into the foreseeable future. It really is like waiting around for Godot. When Financial institution Price was first minimize to .5pc in reaction to the fiscal disaster, marketplaces expected rates to commence increasing yet again in a year. 6 a long time afterwards, Lender Rate is still at .5pc and markets still expect them to rise in a 12 months. In Europe it’s not for 4 years.

Equally Keynsian and monetary economics seem to be to be in some kind of end match. What will come next is anyone’s guess.