When will desire rates rise? The way things are likely, perhaps in no way

Markets, not central bankers, are the root lead to of present-day quite minimal interest charge surroundings, and they demonstrate handful of indications of shifting their view &#thirteen

&#thirteen Image: Howard McWilliam

&#thirteen Image: Howard McWilliam

When will interest charges rise? Not now, which is for confident. Possibly by no means. Alright, so in no way say never, but very most likely not for a long time.

In the Spending budget , the Chancellor announced a tax split for savers. Thanks for that it was much better than a poke in the eye. But as the element of the Spending budget paperwork reveals, at a price of tiny more than £1bn in the very first year, it was a comparatively inexpensive evaluate to enact.

To consider complete gain, as a standard charge taxpayer, of the new £1,000 allowance, you require at current charges of interest a minimum £50,000 in the financial institution, even though admittedly, the numbers really do not seem fairly so complicated if completely invested in publicly subsidised pensioner bonds.

Be that as it may, the real issue for savers is not so significantly the iniquity of double taxation on funds deposits, coupon earnings and dividends – only partly addressed by this evaluate – as extremely lower curiosity prices.

In true phrases, they have in no way been as reduced for this sort of a extended period of time of time. Even in the nineteenth century, when inflation was shut to zero for significantly of the time, true fascination costs routinely accomplished their lengthy-expression common of 2.5pc to 3pc. Traders would eliminate for this kind of a genuine charge of return nowadays.

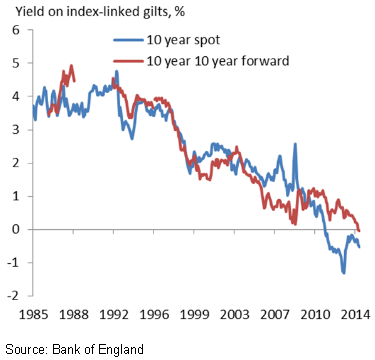

Instead, their selection is progressively constrained to items that hardly preserve tempo with inflation. If recent movements in bond marketplaces are everything to go by, even these will quickly be unavailable. The generate on inflation-linked, 10-year British isles gilts has been negative because 2011, and recently has taken an additional dip downwards on the continent, 5-12 months yields on standard German, Dutch and Swiss bonds have all absent damaging for the first time at any time. Nearly unbelievably, some company bond yields have gone negative, way too. Those who acquire these kinds of bonds are knowingly locking in a specified decline on maturity. We have entered the cloud cuckoo land of actually obtaining to pay out governments, and the most creditworthy organizations, for the privilege of lending to them, a similar dynamic to previous-type, deposit box banking, where you had to shell out the financial institution for keeping your money.

You can blame central bankers and their govt masters for this phenomenon if you like, but the reality is that there are significantly bigger forces at operate here than manipulative, monetary activism.

As Ben Broadbent, deputy governor of the Financial institution of England, put it in a modern speech : “Rather than creating the drop themselves, central financial institutions have as an alternative been accommodating a further downward development in the all-natural, or equilibrium charge of curiosity.”

To Mr Broadbent, central bankers are not so much the instigators of any distinct amount of fascination costs as slaves to what is going on in the wider economic system.

This can’t be fully real, of program. Just recently, for instance, equally the anticipation and later enactment of European Central Lender “quantitative easing” has plainly had a fairly marked result on European bond yields, driving some into unfavorable territory. Without a doubt, lowering bond yields in the hope of persuading investors out of reduced threat into increased danger assets is part of the function of QE. Unconventional monetary coverage has also been exceptionally useful in decreasing the discomfort of fiscal consolidation. Public personal debt has properly been monetised, allowing governments to borrow far more than in any other case, and at significantly reduced curiosity rates, way too.

Nonetheless, it is straightforward to see in which Mr Broadbent is going with the argument. Declining marketplace curiosity prices long pre-day the fiscal crisis and the subsequent age of unconventional financial policy. Back again in the early 90s, the produce on ten-yr, index-connected gilts was close to four.5pc. A 10 years later it experienced fallen to just 2pc. There was no QE at the time. There was also very a bit of yo-yoing all around in each the Fed Funds Rate in the US and Bank Price in the British isles in the course of this interval, so the drop in threat-cost-free marketplace prices can’t genuinely be pinned on the central bankers. One thing else was likely on.

Many triggers have been recommended for this secular drop in prices. The clear explanation is that disinflationary forces in the world financial system have remained remarkably persistent, once again extended preceding the economic disaster. Just as it appears as if these forces may possibly be on the wane, together will come an additional further to preserve inflation minimal – the latest illustration becoming the collapse in the oil value. Andy Haldane, the Financial institution of England’s chief economist, is so concerned by these traits that in a speech on Thursday, he explained plan makers, far from getting ready for a fee hike, ought to maybe be readying on their own for a more reduction . Partly, it may possibly also be about the so-named savings glut, exactly where a combination of ageing demographics and insufficient social welfare has compelled an abnormal diploma of saving in China and a variety of other Asian economies. The consequent surplus may have forced down charges in Western economies.

Another very likely rationalization is that men and women nonetheless worry financial calamity, and are consequently driven into perceived safe havens these kinds of as US Treasuries. The result is to set up a vicious circle of depressed need. Much more cash applied to government bonds signifies more cash saved and significantly less for intake and organization investment decision. If you are of the Thomas Piketty faculty of considered, you may possibly in addition point to increasing inequality, with wealth more and more concentrated in the fingers of the number of and for that reason unavailable for broader use and investment decision in productive activity. In fact, this is a reversal of previous thinking on these issues. The Victorians, for instance, thought that accumulation of capital by the rich was crucial to offer the signifies for productive investment. The evidence possibly way is scarcely conclusive.

Alternatively, the phenonenon may well be attributed to declining costs of efficiency growth. If efficiency is stagnating, at least in sophisticated economies, that’s certain to feed via to reduced rates of return. It also describes sluggish development in median wages, yet another lead to of subdued inflation.

Whatsoever the reasons, the fact is that central bankers are struggling to raise prices from the ground they sunk to in the financial disaster. Even the US Federal Reserve, which is the closest of the foremost central banks to using the plunge, retains putting off the choice. As widely predicted, the Fed’s Open up Markets Committee (FOMC) this week eliminated the term “patient” from its policy guidance . The Fed is no for a longer time heading to be “patient” about boosting charges.

But this didn’t indicate, mentioned Janet Yellen, the chair, that the Fed was now impatient to elevate costs. Marketplaces drew the clear conclusion – that in the face of a significantly much better dollar and recent weakness in the info, the first increase in rates experienced been pushed out right up until the FOMC’s September conference at the earliest. With the eurozone now occupied exporting its possess particular brand of financial contractionism to the rest of the globe, even that day have to be in some question.

It seems scarcely believable that today’s extraordinarily lower rates can rule for really a lot more time. But that’s been the conventional knowledge, cast by the still remembered inflationary 1970s and 80s, for a prolonged time now. Several have misplaced their shirts betting on it. It truly is grow to be like ready for Godot. In his speech, Mr Haldane explained these consistently dissatisfied anticipations of higher prices like this: “In March 2009 US plan rates ended up in a assortment of -.25pc, their cheapest-at any time stage. Marketplaces expected them to increase in a calendar year. In the euro-area, coverage rates were also at all-time lows, but had been anticipated to rise inside 18 months or so. 6 several years on, US plan charges continue to be among -.25pc, whilst euro-area costs are one hundred fifty foundation details reduce. The 1st rise in US policy charges is even now anticipated in a calendar year, although the first increase in euro-area rates is now not envisioned for more than four many years.”

At some point, the worm will switch. As I say, the prolonged-expression indicate for actual fascination prices is in the variety of 2.5pc to 3pc. If you have been questioned the place costs will be in twenty to 30 years from now, this would be a realistic guess. Appropriate now, even so, there is minor sign of the desire and inflation required to produce these kinds of a result.