Germany’s report trade surplus is a larger danger to euro than Greece

If EU regulation had been correctly enforced, Germany would face fines for endangering eurozone steadiness and breaching the Macroeconomic Imbalance Process for the fifth year in a row

&#thirteen

Picture: Reuters

&#thirteen

&#thirteen

Picture: Reuters

&#thirteen

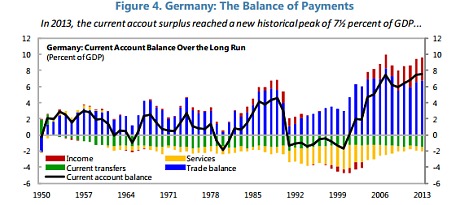

Germany’s current account surplus is out of control. The European Commission’s Spring forecasts demonstrate that it will smash all prior data this yr, achieving a modern day-era large of seven.9pc of GDP. It will even now be 7.7pc in 2016.

Imprecise assurances that the surplus would fall in excess of time have when yet again appear to practically nothing. The place is now the most significant solitary violator of the eurozone steadiness principles. It would confront punitive sanctions if EU treaty law was enforced.

Brussels advised Germany to do its “homework” a calendar year in the past, but recoiled from taking any motion. We will see if Jean-Claude Juncker’s fee does any far better this time.

If not, cynics might justifiably conclude that big international locations perform by their own guidelines in Europe, and that Germany can defy all principles.

The EMU punishment machinery is highly political, in any situation. The story of the EMU financial debt disaster is that the authorities persistently implement a creditor agenda fairly than macro-financial welfare (an fully diverse issue).

This is the fifth consecutive yr that Germany’s surplus has been over 6pc of GDP. The EU’s Macroeconomic Imbalance Method states that the Fee need to launch infringement proceedings if this takes place for 3 many years in a row, unless there is a obvious purpose not to.

There are handful of extenuating circumstances in this circumstance. Germany’s surplus is not induced by a 1-off shock. The surplus continues to be massive even if modified for reduce power import charges. It is a continual structural abuse, rendering financial union unworkable more than time, and is absolutely a lot more hazardous for eurozone unity than anything at all likely on in Greece .

“The European Fee should stop pulling its punches: Germany need to be fined,” explained Simon Tilford, from the Centre for European Reform.

“Their surplus ought to be taken care of in the same way as the southern deficits had been taken care of earlier, as a equivalent threat to eurozone balance. What is so stressing is that the surplus would generally be falling speedily at this stage of the economic cycle,” he said.

Germany’s jobless charge is at a publish-Reunification minimal of 4.7pc. It must for that reason be enjoying a surge of usage. This it is not occurring because the rebalancing system is jammed. What this shows is the EMU remains fundamentally out of kilter, and doomed to lurch from crisis to disaster even if there is a restoration.

Any rebound in southern Europe will lead to the exact same create-up in intra-EMU trade imbalances, and as a result in the very same offsetting capital flows, seller-debt financing, and asset bubbles that led to the EMU crisis in the 1st place.

The International Monetary Fund warned previous 12 months that the German surplus – then 8.25pc of GDP when adjusted for the cycle – is damaging for EMU as a entire. It is between three and 6 share points greater than is either “desirable” or justified by fundamentals. It is not in Germany’s very own economic fascination, and tends to make it even harder for the EMU crisis-states to claw their way out of trouble.

The IMF explained Germany’s exchange price is undervalued by as significantly as 18pc underneath trade elasticity idea even then, prior to the far more current plunge in the euro. This was achieved by squeezing wages in the early years of EMU, undercutting the South.

Attempts by France, Spain, Italy, Portugal and Greece (tremendous-aggressive Eire is irrelevant to this debate) to claw again lost ground by carrying out the exact same at this late phase is precisely what pushed the EMU system as a total into a quasi-deflationary slump from 2011 to 2014.

Germany denies that it is a serial violator of the Macroeconomic Imbalance Procedure. It admits that EMU consequences have left the nation with an undervalued exchange fee but denies that this is the end result of “policy distortions”, allow by itself a deliberate, cynical, self-interested approach of mercantilist exploitation.

It is no secret why the imbalance is acquiring even worse. The German regulatory and tax composition is geared in favour of output and exports, and in opposition to intake. It is the mirror graphic of Britain. Neither system is healthful.

“Germany should lower taxes on lower incomes and VAT. It has lots of fiscal scope to do so. It chooses not to,” mentioned Mr Tilford.

Berlin has refused to offset anemic need with additional authorities paying. The “Ordoliberals” in the German finance ministry are as an alternative working a funds surplus of .6pc of GDP in a around-spiritual glorification of financial savings.

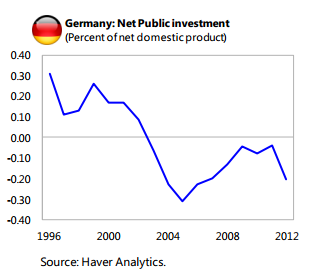

They are doing this even as the Kiel Canal crumbles into the water and Germany’s infrastructure gradually falls aside. Marcel Fratzscher, head of Germany’s DIW Institute, and the writer of Die Deutschland Illusion states investment has fallen from 23pc to 17pc of GDP because the early 1990s. Web public expense has been damaging for 12 several years.

German surpluses did not subject in the times of the D-Mark. The region revalued from time to time, correcting the issue. How Germany ran its possess inside affairs ended up largely its personal business. But as the IMF has frequently said, it is an entirely different issue in a financial union. The German surplus lies at the root of EMU’s North-South divide.

Below the Macro Imbalanced Method – which Germany wrote into regulation pondering it would only at any time be employed in opposition to deficit “sinners” – the eurozone can purchase Germany to present an “action prepare” to cut the surplus. If that fails, EU ministers then sit in judgment on Germany. They can pressure Berlin to pay a deposit of up to .1pc of GDP (€2.4bn) into a specific account, while it is on probation. Eventually, this cash can be seized if absolutely nothing is done.

Useless to say, any such sanction would lead to outrage in the Bundestag and chance destroying German political consent for the euro. Most German citizens already consider that their nation is paying too considerably bailing out southern Europe.

We watch with desire to see how Mr Juncker chooses to navigate these treacherous political reefs, specially since he holds his present occupation by German patronage. It was Chancellor Angela Merkel who shoe-horned him into the Berlaymont previous 12 months from British objections.

With a number of honourable exceptions – this kind of as Mr Fratzscher – the German policy elites refuse to accept that there is anything at all mistaken with their surplus policy, or even that there is any want to discuss the topic at all.

This refusal to see matters from anyone else’s level of see is testing tolerance around the planet. Germany has displaced China as the arch-villain in the US Treasury’s reviews to Congress on currency manipulation, and for apparent factors.

Continual surpluses are a way of thieving demand from customers from elsewhere. They export unemployment to other nations. This matters in an era of “secular stagnation” and surplus world-wide cost savings. Societies are entitled to retaliate after this will get out of hand.

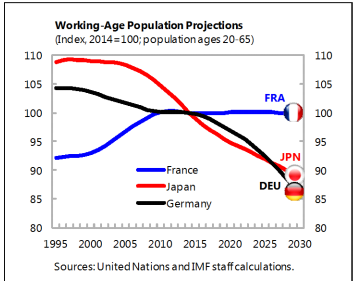

Nor does this mercantilist policy make any feeling for Germany by itself. The surpluses are becoming recycled into money flows abroad with a damaging fee of return, eroding the prosperity foundation that the nation will want above the following ten many years as it goes into precipitous demographic decrease. Historians will look at the Schroder/Merkel era as a series of plan blunders.

The faster Germany abandons fiscal fetishism and invests its very own income in its very own nation for its personal great, the greater it will be for everyone.